Bank Zero has released its pricing guide, which is expected to trigger an intense price war among local financial institutions.

SA’s newest digital-only bank

is preparing to officially launch to the public before the end of this year, after rolling out end-to-end live beta testing last month.In its new pricing guide, described as turning banking

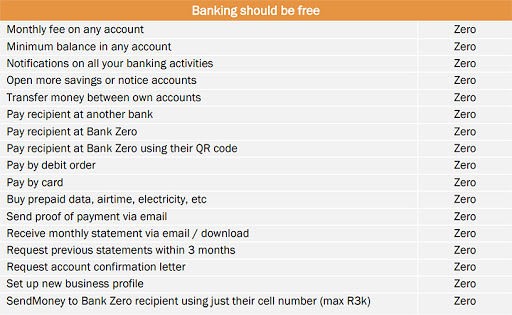

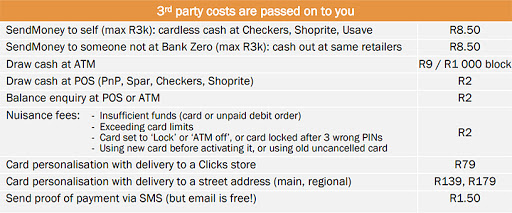

pricing “right way up”, Bank Zero offers free basic banking services. Only extra services are charged for. The bank bills itself as the first bank in SA to charge zero fees for EFT payments. It also offers free debit order services and there is no charge for payments made to other Bank Zero customers.In instances where pricing applies, such as drawing cash at any ATM (R9) and balance enquiry (R2) at a POS or ATM, the same pricing applies to both individuals and all businesses.

The bank says it has no entry-level accounts that often require an upgrade to high-priced accounts, as it offers customers a "segment-agnostic" approach.

Lezanne Human, co-founder and executive director of Bank Zero, explains how the bank is able to offer competitive prices: “We have focused specifically on keeping our own internal cost base low by not spending billions on buying off-the-shelf banking packages, but rather building our own innovative and secure core banking platform.”

Bank Zero, which received its licence one year after competitors TymeBank and Discovery Bank, is co-founded by its seven investors, including former First National Bank CEO Michael Jordaan, who is chairman, and banking innovator Yatin Narsai.

The bank does not have any branches and relies mainly on the mobile app and Web site for sign-ups and transactions. It has partnered with Checkers, Shoprite, Usave, Spar and Pick n Pay to allow customers to draw or send cash to recipients, with transactions charged at R8.50 per transaction. It also has a partnership with Clicks, where personalised

bank cards can be collected by customers.The bank says it will introduce additional partnerships and business investment services such as trusts, at a later stage.

Discussing the bank’s ability to generate profit, Human points out Bank Zero intends generating its income from customers’ account balances and fees.

“The income is derived from account balances such as interest margin that result in interest revenue and fees when customers transact. The six payment rails offer full day-to-day banking and more.

“This means each time a customer transacts, we earn fees like interchange (card, EFT, QR), prepaid commission, cash fees and value-added services. Business banking relies heavily on these transactional services but sadly incur heavy bank charges until now,” she explains.

Bank Zero has received queries from large businesses looking to create partnerships and to unlock synergies with the bank, adds Human.

“We welcome such interest and firmly believe this can create mutual benefit at the right time. For now, we want to solely focus on getting to public operations,” she concludes.